Key Takeaways:

- $30B on-chain, up ~900% from $2.9B in 2022

- Figure, BlackRock, Franklin Templeton, and Paxos among biggest tokenized RWA issuers

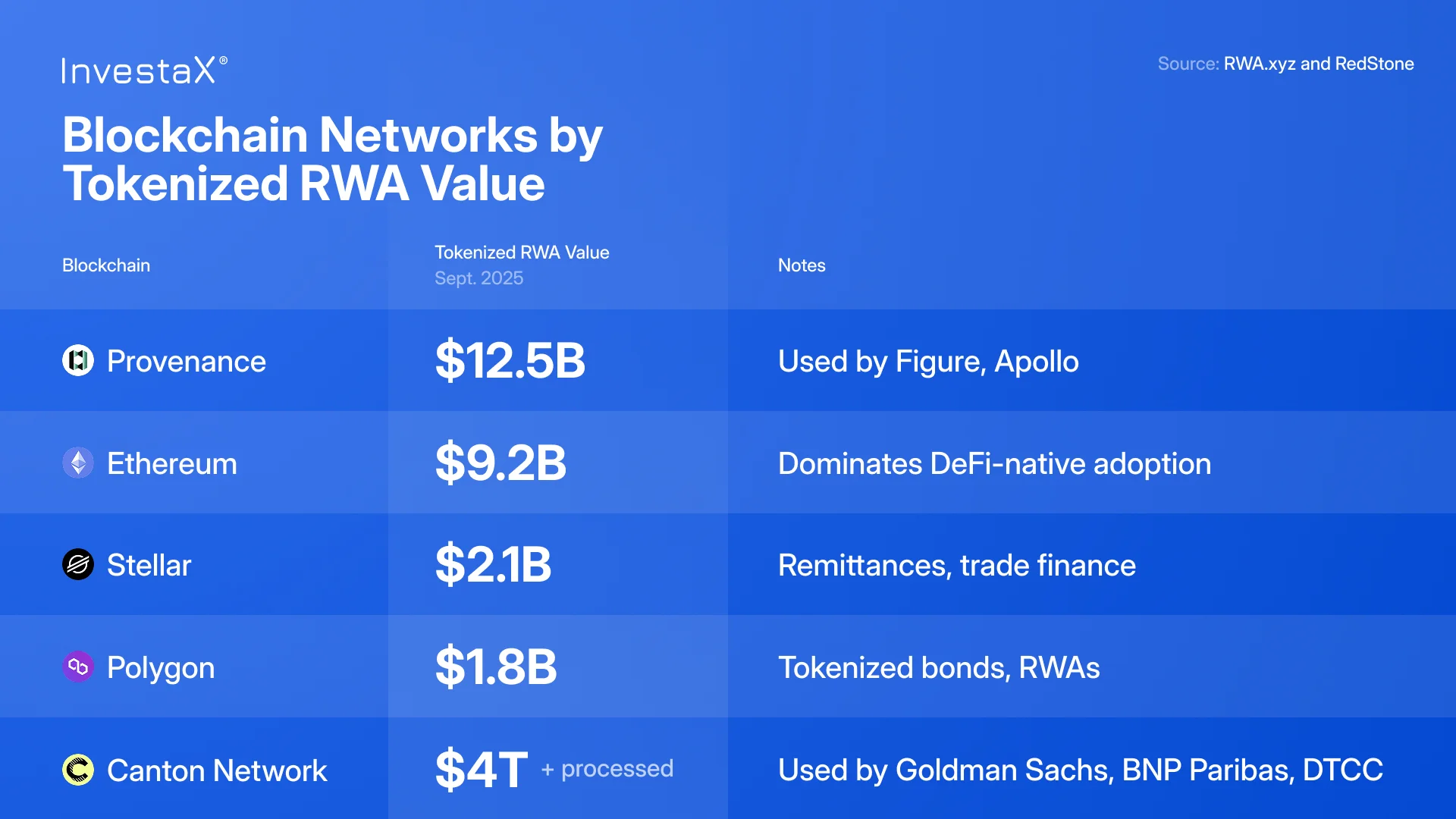

- Provenance hosts $12.5B in tokenized RWAs; Ethereum follows with $9.2B

- Canton Network now processes over $4T in tokenized assets, including $2T/month in U.S. Treasury repo transactions

- Tokenized private credit ($17B) and U.S. Treasuries ($7.3B) are emerging as key categories

- Liquidity, custody, and regulatory harmonization remain under consideration

Tokenized real‑world assets (RWAs) have been the second-fastest growing market in the digital asset space. As of September 2025, total RWA on-chain has exceeded $30 billion in value. This marks a substantial increase from about $2.9 billion three years earlier, growth of approximately 934% (RWA.xyz). Much of this rise is driven by yield‑bearing assets such as private credit and U.S. Treasuries.

Looking ahead, projections remain cautious. A recent study by Ripple and BCG projects that tokenized assets will surge from about $0.6 trillion today to $18.9 trillion by 2033.

The report also suggests that institutions are likely to begin with lower-risk, familiar products such as Treasuries and money market funds, before gradually moving into more complex strategies like private credit that carry higher risk-adjusted returns. [Read more]

This helps explain why Treasuries and private credit are leading today’s tokenization wave. They align with existing institutional preferences: predictability, regulatory clarity, and yield sources that fit into current portfolio construction.

What’s Driving Growth in Tokenized Yield‑Bearing RWAs

For issuers and investors, tokenized yield products offer a pathway to access yield without departing from familiar financial structures, with the added benefit of broader reach, on-chain capital access, expanded utility and improved efficiency

- Wider distribution potential

Traditional income generating vehicles are often subject to local fundraising rules and restricted to a narrow group of institutional investors. Tokenization introduces new flexibility by making these financial instruments digital, divisible, and transferable, opening the door for more efficient distribution to qualified investors.

Regulated RWA platforms like InvestaX provide the infrastructure, compliance tools, and licensing framework such as Singapore’s Capital Markets Services (CMS) to help issuers expand beyond their distribution reach. By combining tokenization technology with regulatory oversight, issuers can diversify and grow their investor pool in a compliant and scalable way.

- On-chain capital readiness

The stablecoin market, now valued at over $290 billion, represents a liquid, programmable source of capital. By allocating directly into tokenized yield strategies, investors can deploy funds without conversion to fiat or reliance on traditional intermediaries. This creates an efficient bridge between stablecoin liquidity and regulated yield products.

- Expanding collateral use cases

Yield-generating RWAs are also being integrated into institutional workflows. For example:

- Standard Chartered and OKX now use tokenized MMFs as collateral in settlement processes.

- MakerDAO allocates hundreds of millions of dollars into tokenized Treasuries to back DAI.

- Binance supports tokenized Treasuries as margin collateral.

These examples show that tokenized RWAs are not only held passively, but also increasingly serve operational roles in collateral management and treasury functions.

- Operational benefits and auditability

Tokenization also has potential for operational efficiency improvements. Tokenization enables on-chain servicing logic, real-time cap table tracking, and transparent audit trails. This is particularly useful in cross-border or multi-investor structures, where token-based compliance logic can automate restrictions on geography, investor type, and holding periods.

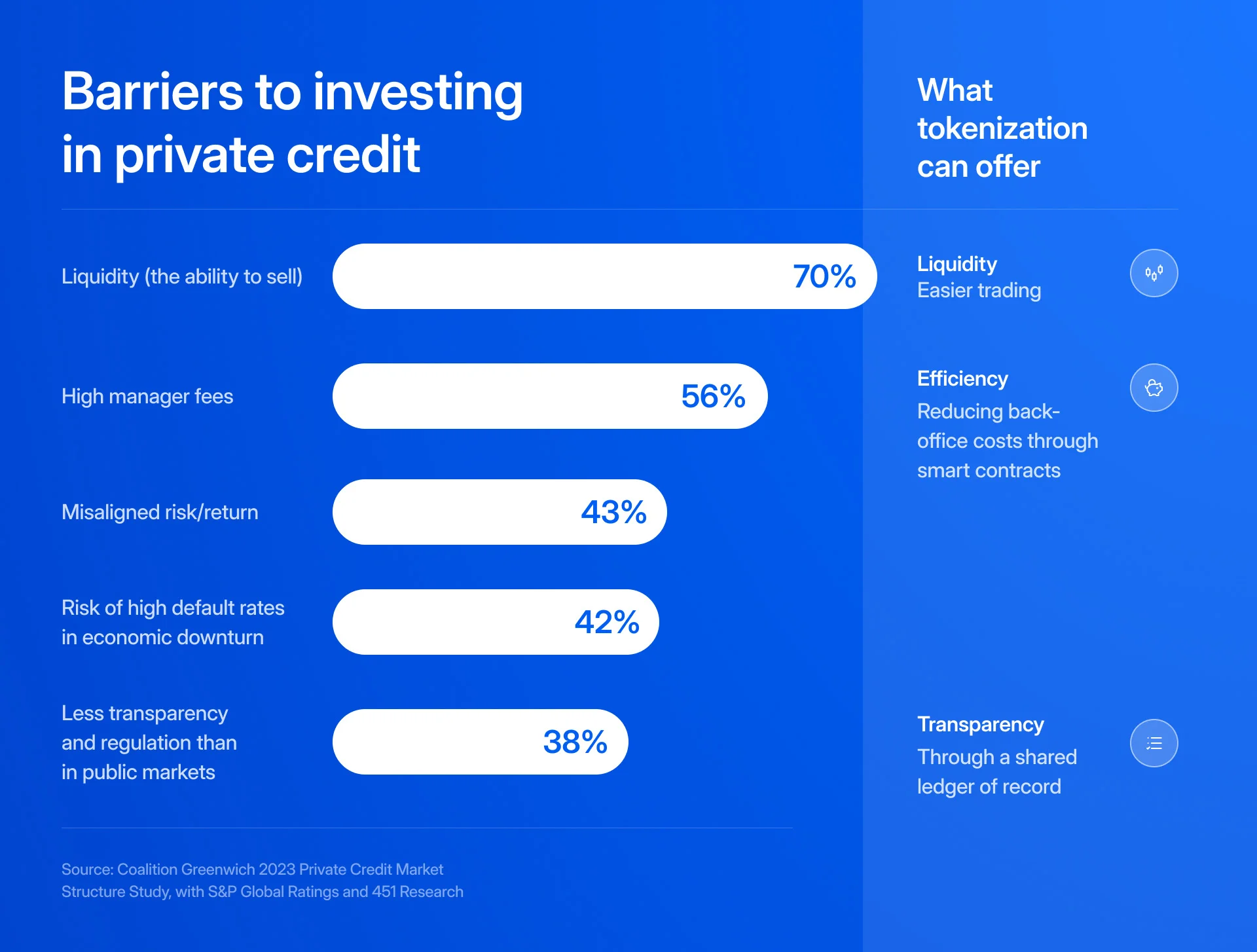

Why Private Credit Is Taking the Lead

With approximately $3.2 trillion in assets under management globally (EY, 2025), private credit has become one of the largest segments in private markets. Yield profiles typically range between 8-12%, depending on structure and risk level. Because the asset class is already familiar to institutions, it is a natural candidate for early tokenization pilots.

Importantly, tokenization is helping reshape how liquidity is designed in private credit. Traditional structures often lock investors in for 5 to 10 years. By contrast, several tokenized vehicles are introducing shorter time horizons and more flexible redemption features. For example:

- Mikro Kapital ALTERNATIVE eNote™, available on platforms like InvestaX, offers SME-linked credit exposure with tenors around 6 to 12 months.

- TradeFlow Tokenized Trade Finance Bond enables exposure to short-term, insured commodity finance, typically with tenor around 6 to 12 months.

These models do not remove the underlying risks of credit, but they illustrate how tokenization can help adapt private credit into more flexible, digitally native formats that remain aligned with institutional standards.

Also read: The Institutional Guide To Tokenizing Private Credit

Tokenized Treasuries: Bringing Familiar Yield On-Chain

If private credit is the breakout category, U.S. Treasuries remain the anchor. With more than $8 billion in tokenized Treasury assets now circulating on public chains, they have become the de facto reserve instrument of the on-chain economy.

This trend mirrors what we see in traditional finance: Treasuries are the backbone of short-term capital markets. They are liquid, familiar, and regulatory-compliant. In digital markets, the appeal is amplified. Tokenized Treasuries allow stablecoin issuers, DAOs, fintechs, and even family offices to move idle capital into yield-producing instruments without leaving the on-chain ecosystem. In practice, this means a USDC or USDT holder can deploy capital into a short-duration, tokenized Treasury note with daily settlement and transparent terms. When markets are volatile, that level of flexibility matters.

We’ve also seen tokenized Treasuries being used in repo markets, in settlement flows, and increasingly, as base assets for new forms of collateralization. For example:

- A consortium led by Digital Asset and DTCC completed a repo financing using tokenized U.S. Treasuries on Canton Network, with USDC as the cash leg and atomic on-chain settlement (including outside normal trading hours).

- JPMorgan’s Kinexys settled U.S. Treasuries tokenized via Ondo Finance on a public blockchain using a delivery-vs-payment structure.

The convergence is already happening.

The Role of Blockchain Infrastructure

While most headlines focus on Provenance and Ethereum, the RWA market today is distributed across both public and permissioned chains.

Provenance Blockchain currently leads in terms of tokenized RWA value, with over $12 billion in assets. Ethereum follows closely with roughly $9.2 billion, hosting many of the most visible players including Blackrock, Ondo, Backed, and Franklin Templeton’s tokenized fund. But perhaps the most underappreciated development is happening on institutional infrastructure rails.

According to RedStone’s “Real-World Assets in Onchain Finance Report,” Canton Network, for example, is now processing more than $4 trillion in tokenized asset volume, including $2 trillion per month in tokenized Treasury repo transactions. This is a permissioned network backed by institutions like Goldman Sachs, BNP Paribas, and DTCC. It represents a structural shift in how regulated market infrastructure is built.

In short, the infrastructure layer is becoming more modular. Public and private chains are being used selectively depending on product type, jurisdiction, and counterparty profile.

What’s Still Developing?

Despite the growth, it’s worth being clear-eyed about where things stand.

- Liquidity

Liquidity remains an area that still needs to be worked out. While tokenized RWAs have seen strong inflows, most of that capital is still held passively, and secondary trading volumes remain limited (arXiv:2508.11651). That suggests institutions continue to use tokenization for operational benefits apart from liquidity aggregation.

- Regulation

Regulatory alignment remains a work in progress. Jurisdictions like Singapore, Switzerland, and the EU have taken important steps, but globally, rules are still fragmented. Issuers, custodians, and platforms often face a patchwork of requirements when operating across borders. That creates friction not just in legal structuring, but in ongoing compliance and product design.

- Custody Infrastructure

Custody is another common concern, especially for institutions new to on-chain finance. The question often comes up: what happens if I lose my wallet key? But the solution already exists. Instead of self-custody, most institutional flows today are handled through regulated custodians. For instance, at InvestaX, we’ve worked with regulated custodians like Cactus Custody to secure users’ assets.

These challenges - liquidity, regulatory clarity and custody infrastructure - are real. But they’re not fixed limitations. They’re the kinds of problems that become solvable as soon as the industry acknowledges them clearly and builds around them. And that process is already underway.

What Comes Next

The milestone of $30 billion shows that tokenized yield assets are now operating at scale, in categories that align closely with institutional priorities: predictable returns, regulatory clarity, and established yield sources.

At the same time, tokenization should be seen as an enhancement to financial infrastructure rather than a change to asset fundamentals. Outcomes still depend largely on asset quality and structure. Within that frame, tokenization can improve servicing, increase transparency, and streamline distribution when compliance and optional liquidity are built into the design.

InvestaX provides institutions with a regulated asset tokenization platform to help them integrate tokenized assets into their strategies. Contact us to get started.