The $3.2T private credit market remains a critical pillar in institutional portfolios, valued for its yield stability, negotiated terms, and low correlation to public markets. But certain elements, such as manual servicing workflows, limited secondary trading, and jurisdictional fragmentation, can limit scale and efficiency.

That’s where tokenization offers potential. By applying programmable infrastructure to existing legal frameworks, institutions may be able to simplify operations, automate compliance, and selectively introduce controlled liquidity.

This guide walks through how private credit can be tokenized using licensed infrastructure, covering structure, risk controls, regulatory requirements, and implementation models.

Private Credit and What Tokenization Unlocks

Private credit refers to non-bank lending across structures like direct loans, asset-backed finance, and trade receivables. These instruments are typically negotiated bilaterally and held by institutional investors seeking yield and control.

Investor demand has grown steadily. Private credit strategies targeting 8-14% unlevered yields continue to attract allocations from insurers, sovereign funds, private banks, and family offices. But scale can be hard to achieve when workflows are fragmented. Inefficiencies in servicing, capital deployment, and reporting limit access and scalability. Onboarding, KYC, interest payments, and secondary sales often rely on legacy systems.

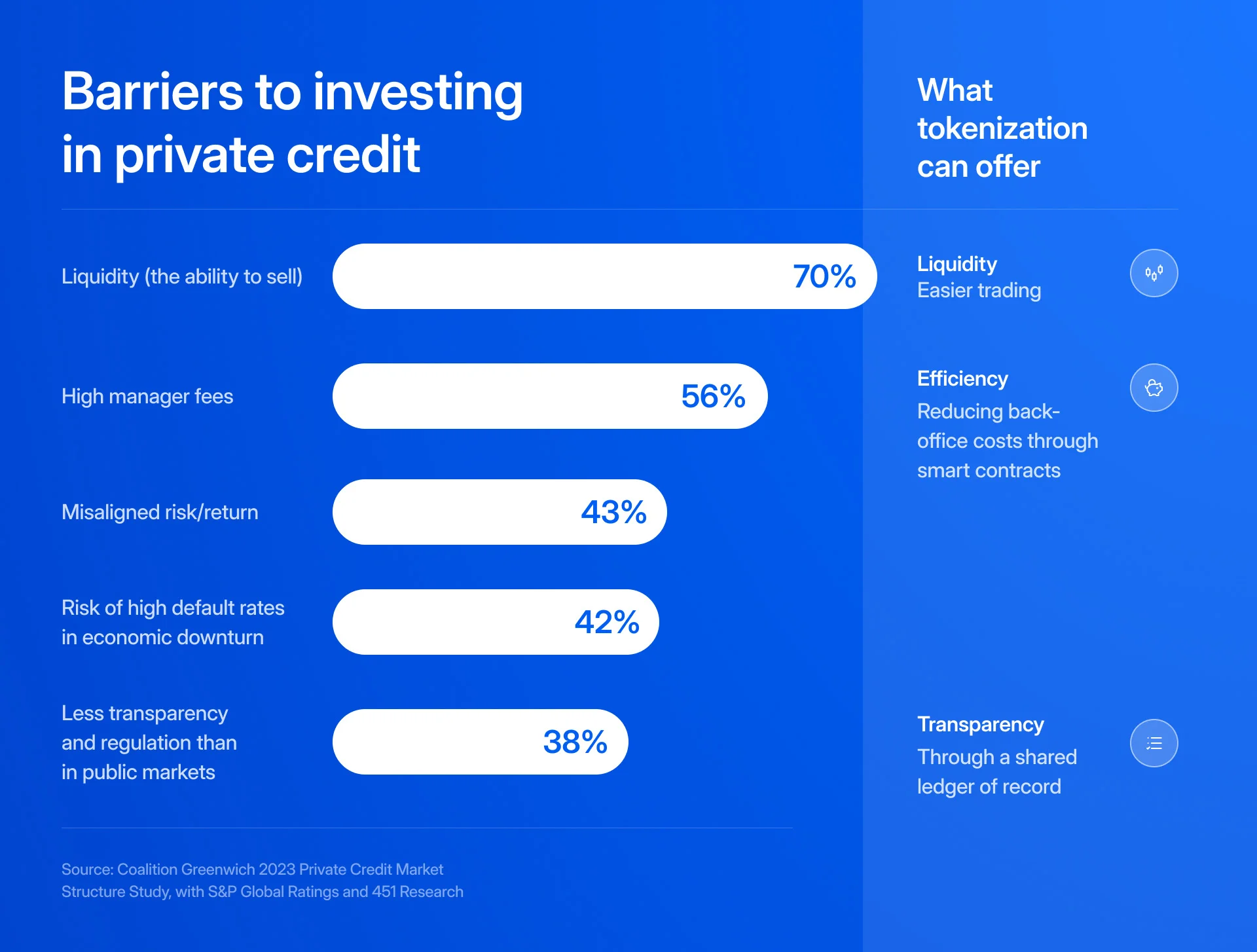

According to S&P Global, liquidity, transparency, and operational burden are among the top barriers to investing in private credit. And tokenization offers tools that align with these challenges.

- Operational efficiency

Tokenization can leverage smart contracts and distributed ledgers to streamline issuance, settlement and asset servicing. According to the Impact of Distributed Ledger Technology in Capital Markets report by BCG and GFMA, tokenized bond settlements can occur nearly instantly (T+0), compared to multi-day cycles in traditional systems.

- Liquidity Options

While many private credit structures are designed to be held to maturity, tokenization can offer selective liquidity, including redemption windows or access to regulated secondary venues. For example, OpenTrade structures allow daily redemption through tokenized vaults backed by treasury assets. Regulated secondary platforms such as IXS DEX and InvestaX are beginning to facilitate trading windows for tokenized private credit within licensed parameters.

- Transparency

Tokenized assets record all transactions immutably on-chain, offering institutions enhanced visibility into investor holdings, payment flows, and transfer history. This data can support reconciliation, real-time audit trails, and compliance reporting, particularly in multi-jurisdictional structures where investor oversight can be fragmented.

Private Credit as The Largest Tokenized Segment

Private credit is now the largest segment in the tokenized real-world asset (RWA) space. As of September 2025, it accounts for over $16 billion of the $28 billion tokenized RWA market, according to rwa.xyz.

While still small relative to the $3.2 trillion traditional private credit market (EY, 2025), tokenized credit has grown more than 74% over the past 12 months.

The segment’s expansion aligns with two parallel developments.

- First, institutional demand for fixed‑income instruments with yield enhancement remains strong. Tokenized private credit normally offers 8-14 percent yields, which are attractive compared to public debt instruments.

- Second, the infrastructure to support token issuance, compliance, and asset servicing has matured. This enables scalable deployment outside pilot contexts.

Yet, it’s important to note that tokenized private credit remains shaped by its broader ecosystem. Despite growing capital inflows, on‑chain liquidity is seen as limited (arXiv:2508.11651), with many tokens showing low trading volumes and passive holding patterns. That suggests institutions continue to use tokenization for operational benefits such as faster settlement and compliance automation, apart from liquidity aggregation.

Real-World Use Cases of Tokenized Private Credit

Across sectors and regions, institutional and alternative lenders are adopting tokenized private credit structures to improve access, servicing, and investor distribution. Below are several examples that illustrate how tokenization is being applied in practice.

SME Lending in Emerging Markets

Example product: Mikro Kapital ALTERNATIVE eNote™

This is a tokenized fixed-income instrument structured to channel capital into microfinance and SME lending across Eastern Europe, MENA, and Central Asia. The eNote provides investors with exposure to diversified private credit portfolios via digital distribution, while the underlying loans are originated and managed off-chain. The structure targets yields of up to 9.5% p.a., with tokenization used to streamline access and servicing.

Mikro Kapital ALTERNATIVE eNote™ is available through the InvestaX platform. Learn more here.

Short-Term Trade Finance

Example product: TradeFlow Tokenized Trade Finance Bond

This instrument tokenizes short-term, insured commodity trade finance transactions. It is structured to offer exposure to real-world trade flows with maximum tenors of 90 days. The tokenized format is used to automate recordkeeping and enhance transparency, while the underlying credit remains managed within conventional finance and insurance channels. Target yields are around 8.5% p.a.

TradeFlow’s fund is available through the InvestaX platform. Learn more here.

Emerging Market Lending via Decentralized Protocols

Example project: Goldfinch

A credit protocol providing over $100 million in active loans across 20+ countries. Loans are originated off-chain, while investor exposure is managed through tokenized instruments and smart contract-based repayments.

How to Tokenize Private Credit: A Step-by-Step Guide

For institutions new to tokenization, the process generally follows a structure you may already be familiar with. You still originate loans, structure SPVs, and serve institutional investors. What changes is how these assets are issued, serviced, and accessed using programmable infrastructure that operates within existing legal frameworks.

The below flowchart applies to tokenising bonds - which is a specific financial instrument through which private credit is raised.

.avif)

This section walks through each stage of the tokenized private credit lifecycle.

1. Structure the Deal

You originate or source a private credit instrument, for example, a direct loan, asset-backed facility, or SME financing pool. This is typically placed in a Special Purpose Vehicle (SPV) or similar entity.

What you need to plan for

- Choose the jurisdiction and structure of the SPV

- Draft legal documentation that can support digital issuance (e.g. Bond Agreements, Notes, shareholder agreements , payment terms)

- Consider tax treatment, segregation of assets, and cross-border enforceability

The SPV remains the legal owner of the loan. The token will later represent an interest in this structure, so clarity here sets the foundation for enforceable, compliant issuance later.

Also read: Real World Asset Tokenization - Is A License Needed?

2. Create the Tokenized Instrument

The SPV’s participation units are converted into digital tokens that represent an interest in the underlying credit. These tokens are structured to comply with securities regulations.

What you need to plan for

- Decide the type of token (e.g., equity interest, debt instrument, profit-sharing note)

- Select the blockchain network (Ethereum, Polygon, etc.)

- Embed compliance controls like whitelisting or transfer restrictions

- Prepare investor documents (bond agreements, notes, subscription agreements, offering memorandum)

Compliance considerations

Tokens issued to accredited or institutional investors are often structured under private placement exemptions. These are jurisdiction-specific and may limit how broadly you can offer the asset.

To reduce operational heavy lifting, you can work with regulated tokenization platforms like InvestaX. InvestaX with a Capital Markets Services (CMS) and Recognized Market Operator (RMO) licenses issued by the Monetary Authority of Singapore offers compliant issuance, smart contract tools and integration with regulated custodians.

3. Onboard and Allocate to Investors

Qualified investors subscribe to the token offering. They complete onboarding, provide KYC/AML documents, and receive tokens in their wallets.

What you need to do:

- Verify investor accreditation and jurisdictional eligibility

- Collect KYC/AML documentation

- Allocate token subscriptions and settle funds

- Deliver tokens to whitelisted, custodial wallets

Compliance considerations

Investor eligibility checks are critical and must comply with your offering regime. Transfers can also be restricted at the smart contract level to maintain compliance across the token’s lifecycle.

Platforms like InvestaX, which integrates with KYC software providers like ComplyCube for KYC/AML checks, help simplify onboarding and wallet issuance by integrating identity checks, investor dashboards, and audit trails. This reduces manual back-and-forth while maintaining auditability.

4. Service the Tokenized Instrument

Throughout the life of the deal, you’ll need to service the instrument, such as paying interest, updating investor records, and maintaining reporting flows.

What you need to do:

- Monitor loan performance and update any payment schedules

- Distribute interest and principal via smart contracts or mirrored off-chain processes

- Maintain audit trails and investor reporting

- Manage cap table and transaction history

Smart contracts can automate interest distributions, cap table updates, and recordkeeping. On-chain data gives you real-time transparency while maintaining consistency with your legal structure.

5. Provide Liquidity or Redemption Options (If Applicable)

Depending on the structure, the tokens may be redeemable at certain intervals or traded on secondary markets within regulatory constraints.

What you need to do:

- Define redemption rights and windows in offering terms

- Monitor NAV or fair value (if required)

- Coordinate settlement flows and investor notifications

- If enabling trading, list on a licensed secondary platform or work with regulated brokers

Compliance considerations

In many jurisdictions, only licensed entities can operate secondary markets. Transfers should also comply with securities law and investor protection rules.

To enable compliant liquidity, issuers can work with regulated trading venues like IXS DEX (regulated under the DARE framework in The Bahamas) or use the Recognized Market Operator license at InvestaX for controlled secondary trading access.

6. Close, Reinvest, or Extend

At maturity or after a liquidity event, capital is returned to investors, reinvested into new deals, or rolled into subsequent token offerings.

What you need to do:

- Settle final payments and capital returns

- Redeem outstanding tokens

- Provide final reports and audit materials

- Close the SPV or transition capital

Most regulated tokenization platforms retain complete lifecycle data, which simplifies closing processes, investor reconciliations, and audits.

Key Considerations

As institutions evaluate tokenized private credit, three areas often require the most scrutiny: legal structuring, custody setup, and liquidity planning. Each needs to be addressed early to ensure regulatory alignment and operational readiness.

1. Utility

Tokenization can improve how assets are serviced, distributed, and recorded. But it doesn’t transform the economic fundamentals of the asset itself.

If the underlying credit lacks investor demand, digital wrappers will do little to change that. As with traditional credit, utility generally depends on the strength of the yield, borrower quality, and structure. Tokenization should be seen as an enabler instead of a rescue strategy.

2. Legal Clarity

The regulatory landscape for tokenized assets is still evolving. Depending on the jurisdiction, structure, and investor type, tokenized private credit may need to comply with existing securities laws, prospectus regimes, or private placement exemptions.

To reduce risk, many issuers work with licensed platforms like InvestaX, which supports SPV-backed issuances under a Capital Markets Services (CMS) license and Recognized Market Operator (RMO) status granted by the Monetary Authority of Singapore.

3. Custody

Institutions generally avoid self-custody setups. Instead, tokens are held through regulated custodians offering segregated wallets, institutional onboarding, and multi-signature controls.

Platforms like Cactus Custody and BitGo provide this infrastructure. InvestaX integrates directly with Cactus Custody, so assets are secured in a compliant, auditable environment from day one.

4. Liquidity

Liquidity needs vary by structure. Some tokens are designed to be held to maturity. Others offer redemption windows or limited trading access.

To offer liquidity without regulatory exposure, issuers can structure optional redemptions or use licensed secondary venues like IXS DEX, which allows institutions to explore liquidity within defined parameters.

About InvestaX

InvestaX is a leading institutional-grade platform specializing in the compliant tokenization and distribution of real-world assets (RWAs) globally. Regulated by the Monetary Authority of Singapore (MAS), InvestaX enables financial institutions and asset managers to compliantly issue, manage, and trade tokenized RWAs across a network of fintech platforms, exchanges and distribution partners.

Looking to issue tokenized private credit? Contact us to get started.